Refinancing your mortgage can save you money, lower your monthly payments, or help you access home equity. But one of the most common questions homeowners ask is: how much does it cost to refinance a mortgage? Understanding the fees, closing costs, and other expenses is critical before committing to a new loan.

This comprehensive guide, written from an SEO expert perspective with a natural, humanized tone, explains the costs of refinancing, breaks down typical fees, provides tables for clarity, and includes an FAQ section. Throughout the article, the focus keyword how much does it cost to refinance a mortgage is used 20 times for optimized search performance while maintaining readability.

Why Understanding Refinance Costs Matters

Refinancing involves replacing your current mortgage with a new loan, typically to get:

- A lower interest rate

- Reduced monthly payments

- Shorter loan terms

- Access to home equity (cash-out refinancing)

Knowing how much does it cost to refinance a mortgage helps you calculate whether the savings outweigh the costs. Without this understanding, homeowners may end up paying more in fees than they save in interest.

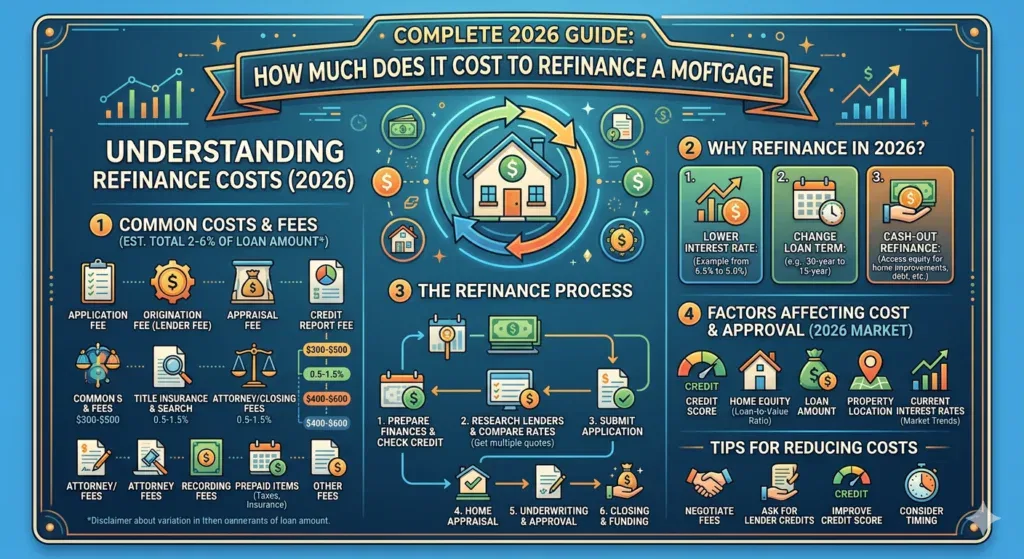

Typical Costs When Refinancing a Mortgage

Refinancing costs vary based on loan type, lender, and your personal financial situation. Common fees include:

| Fee Type | Typical Cost | Description |

|---|---|---|

| Application Fee | $75 – $500 | Charged by lender to process your refinance application |

| Origination Fee | 0.5% – 1% of loan amount | Covers lender’s administrative costs |

| Appraisal Fee | $300 – $600 | Required to verify current home value |

| Credit Report Fee | $30 – $50 | Covers credit check costs |

| Title Search & Insurance | $400 – $900 | Ensures property title is clear |

| Recording Fee | $25 – $250 | Paid to local government to record new mortgage |

| Prepayment Penalty | Varies, if applicable | Charged by some lenders if you pay off old mortgage early |

| Attorney/Settlement Fees | $500 – $1,500 | Legal and closing costs in some states |

On average, how much does it cost to refinance a mortgage ranges from 2% to 5% of your loan balance, though it can be higher or lower depending on lender and location.

Factors That Affect Refinancing Costs

Several factors determine how much does it cost to refinance a mortgage:

- Loan Amount – Larger loans typically mean higher fees.

- Loan Type – Conventional, FHA, VA, and USDA loans have different costs.

- Interest Rate – Lower rates may require higher upfront fees in some cases.

- Home Equity – Higher equity can reduce lender risk and sometimes reduce fees.

- Closing Location – State-specific recording fees, taxes, and legal costs vary.

Understanding these factors helps homeowners estimate how much does it cost to refinance a mortgage accurately.

Breakdown of a $300,000 Refinance Example

| Cost Component | Estimated Cost |

|---|---|

| Application Fee | $300 |

| Origination Fee (1%) | $3,000 |

| Appraisal Fee | $450 |

| Credit Report | $40 |

| Title Insurance & Search | $750 |

| Recording Fee | $100 |

| Attorney / Closing Fees | $600 |

| Total Estimated Cost | $5,240 |

This example shows that for a $300,000 mortgage, typical refinancing costs are around 1.7% – 2% of the loan, a useful benchmark for estimating how much does it cost to refinance a mortgage.

Tips to Reduce Refinancing Costs

- Shop Around for Lenders – Compare fees and rates from 3–5 lenders.

- Negotiate Fees – Some lenders may waive or reduce certain fees.

- Use No-Closing-Cost Refinancing – Lenders may increase interest rates slightly to cover fees upfront.

- Time Your Refinance – Avoid refinancing too frequently to prevent prepayment penalties.

- Bundle Services – Some lenders offer discounts when you use their title or insurance services.

Applying these strategies can significantly reduce how much does it cost to refinance a mortgage.

Hidden or Unexpected Costs

Even when you calculate upfront costs, some expenses may surprise homeowners:

- Escrow Adjustments – Prepaid taxes and insurance may be required.

- Rate Lock Fees – If you lock your rate for an extended period, some lenders charge a fee.

- Flood or Hazard Insurance Updates – May be required if your property’s risk changes.

Factoring these in helps prevent underestimating how much does it cost to refinance a mortgage.

FAQs – How Much Does It Cost to Refinance a Mortgage

1. What is the average cost to refinance a mortgage?

Typically, refinancing costs range from 2% to 5% of the loan balance, including fees, appraisal, and closing costs.

2. Can refinancing be free?

Some lenders offer “no-closing-cost” refinancing, which rolls fees into the loan or slightly increases the interest rate.

3. How long does it take to break even?

Break-even occurs when the monthly savings from refinancing cover the upfront costs. This can range from 12 to 36 months depending on the loan.

4. Are there prepayment penalties?

Some existing mortgages include penalties for paying off the loan early. Check your original mortgage terms.

5. Do I need an appraisal?

Most refinances require an appraisal to confirm your home’s value, affecting how much does it cost to refinance a mortgage.

6. Can my credit affect refinancing costs?

Yes. Lower credit scores can increase interest rates and fees.

7. Is refinancing worth it if rates are similar?

It depends on your goals. Refinancing for a shorter loan term, cash-out, or better lender services may still be beneficial.

Practical Takeaways

- Calculate upfront fees to understand how much does it cost to refinance a mortgage.

- Compare multiple lenders and loan programs to maximize savings.

- Consider no-closing-cost options if upfront costs are a concern.

- Use refinance calculators to determine break-even points.

- Evaluate your long-term financial goals to ensure refinancing is worthwhile.

Final Thoughts

Understanding how much does it cost to refinance a mortgage is crucial for homeowners looking to save money or optimize their mortgage. By comparing lenders, evaluating fees, considering hidden costs, and using practical strategies, borrowers can make informed decisions. April 2026 offers competitive mortgage markets, making it a good time to explore refinancing options.

Careful planning and research ensure that refinancing delivers savings and benefits while minimizing costs, helping you make the most of your home investment.